Most people believe the best way to become a gym owner is: get a loan, find a space, build it out, buy equipment, and pray to the marketing gods that people show up before the money runs out.

This approach usually requires $100,000+ to get up and running, followed by 6-12 money-losing months before the owner breaks even (if they’re lucky).

But what if I told you that with $100,000, you could have a profitable gym that pays over $10k/mo from day 1.

Better yet, what if I showed you how with a bit more money, you could also get millions of dollars of real estate as well.

Buckle up gym owners—you’re about to learn exactly how you can build wealth fast using other people’s money.

Buying a profitable business

You absolutely can spend hundreds of thousands building a gym from scratch. That’s what I did, until I discovered that buying an existing gym is less risky AND more lucrative.

Let me show you why.

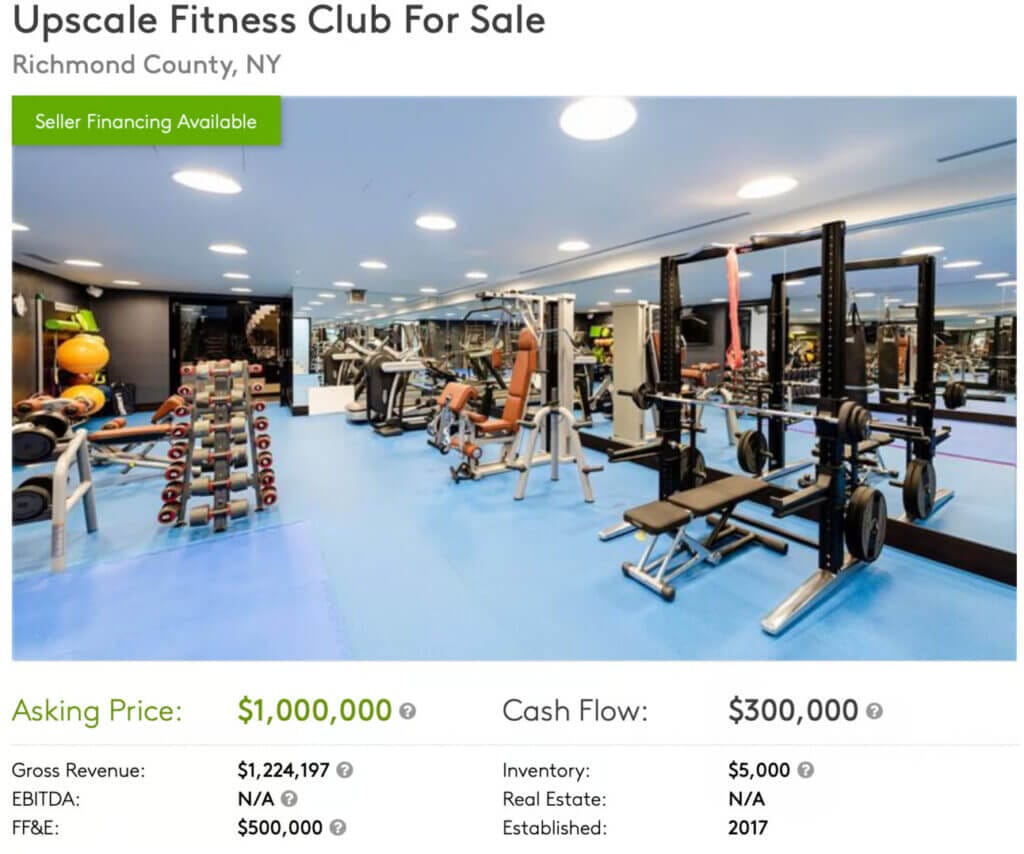

Check out this gym for sale in New York:

It’s doing around $100k a month in revenue and cash flowing about $25k a month.

Here’s how you could own this business for $100,000 and take home $13,000 every month.

Introducing the SBA 7(a) loan

The Small Business Administration (SBA) helps current and aspiring U.S. small business owners access capital they wouldn’t be able to get from a traditional bank. The 7(a) loan is the least restrictive loan, and most people can access up to $5M in capital as long as they have a credit score of 650+, no past bankruptcies, and some business experience.

You can use the money to buy a business, expand your current business, or buy real estate.

The amount of money you qualify for depends on the amount of cash flow your business—or the one you’re buying—generates.

Basically, the business needs to generate enough cash flow to pay for itself.

The fancy banking term for this called the debt service coverage ratio.The ratio is calculated by taking the cash flow a business generates and dividing that number by the amount of money needed to service the debt you’re taking on.

So let’s say your gym generates $20k a month in cash flow and you want to take out a loan where the monthly payment is $10k. In this case, the debt service coverage ratio is 2 ($20k cash flow / $10k debt payment).

We spoke with Live Oak Bank—the largest SBA lender in US—and they told us the debt service coverage ratios they use:

If you’re buying real estate, the ratio is 1:1—so to service $1 of debt payment, the business needs to generate $1 of cash flow.

If you’re buying a business, the ratio is 1.15:1—so to service $1 of debt payment, the business needs to generate $1.15 of cash flow.

So different assets have different coverage ratios. They also have different loan terms.

If you’re buying a business, you have to pay off the loan in 10 years. If you’re buying real estate, you have to pay off the loan in 25 years.

Back to our gym example

So let’s look at our listing again:

The asking price for this business is $1M.

Like a house or a car loan, the SBA requires a down payment—which is usually around 10% of the deal.

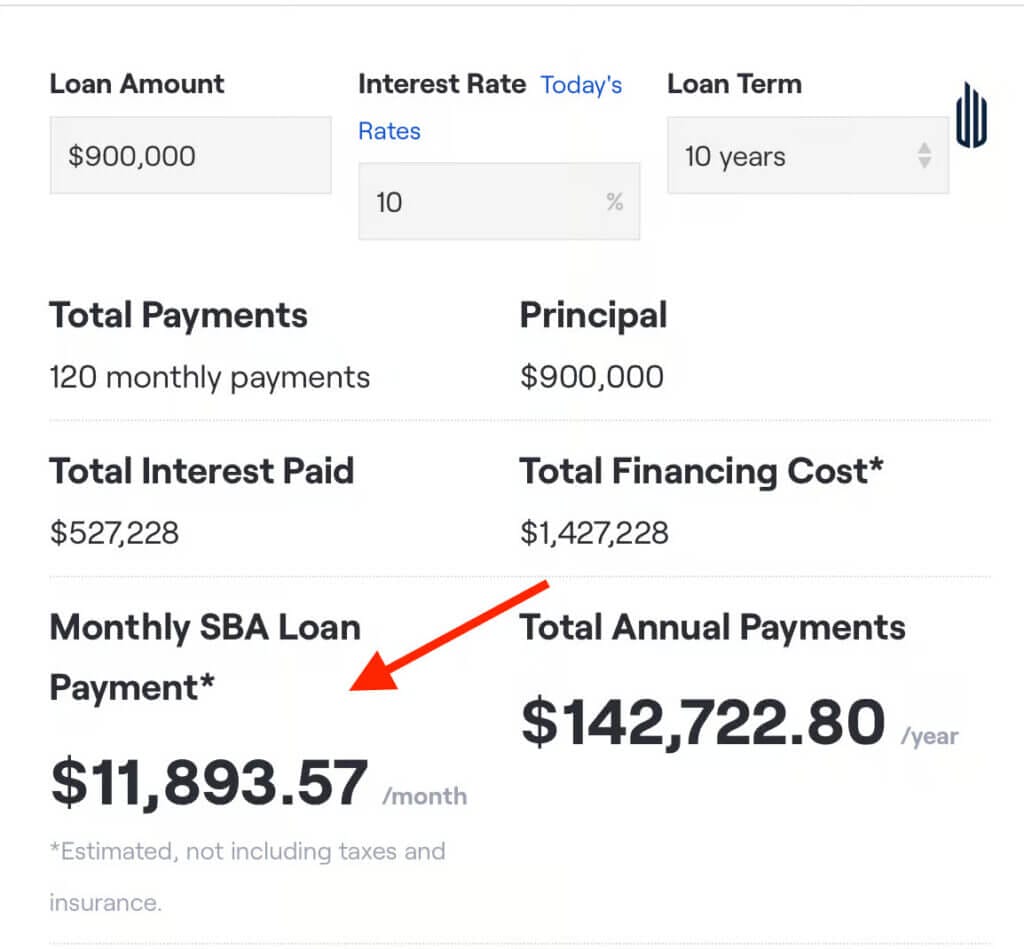

So in this case, you’ll need to come up with $100k (10% of $1M) and the SBA will cover the remaining $900k IF the business meets the 1.15:1 debt service coverage ratio.

We can use this fancy calculator to find out if it does:

Using an interest rate of 10%, we find that it’ll cost around $12k/mo to cover $900k of debt.

We know that the gym brings in $25k/mo in cash flow.

So $25k/mo in cash flow / 12k/mo to service the debt = a coverage ratio of ≈2. This is well above the required 1.15:1 ratio—so the business is financeable. Woo-hoo.

So let’s recap:

→ The biz costs $1M.

→ You pay $100k out of pocket for the down payment.

→ You borrow the remaining $900k from the SBA at a rate of $12k/mo.

→ The biz generates $25k/mo, so after you pay the SBA, there is $13k/mo in cash flow leftover that you get to keep.

So from day 1, you’re making $13k/mo as a gym owner (≈4x more than the average gym owner), plus you’re building equity in the business as you pay down the loan.

This is why I’d never start a gym from scratch again. It’s less risky to buy because you bypass the whole startup phase.

But wait… there’s more 😳

Buying a $1M gym

I talked to Angelo Medici, a senior VP at Live Oak Bank, and he shared a wealth-building hack that I didn’t know about.

If you purchase a business that comes with real estate, the term of the ENTIRE LOAN is 25 years.

The longer loan term makes the monthly payments smaller, which means you can take on more debt.

Luckily for us, the owner of the $1M gym is also selling the real estate.

This is what purchasing both assets would look like:

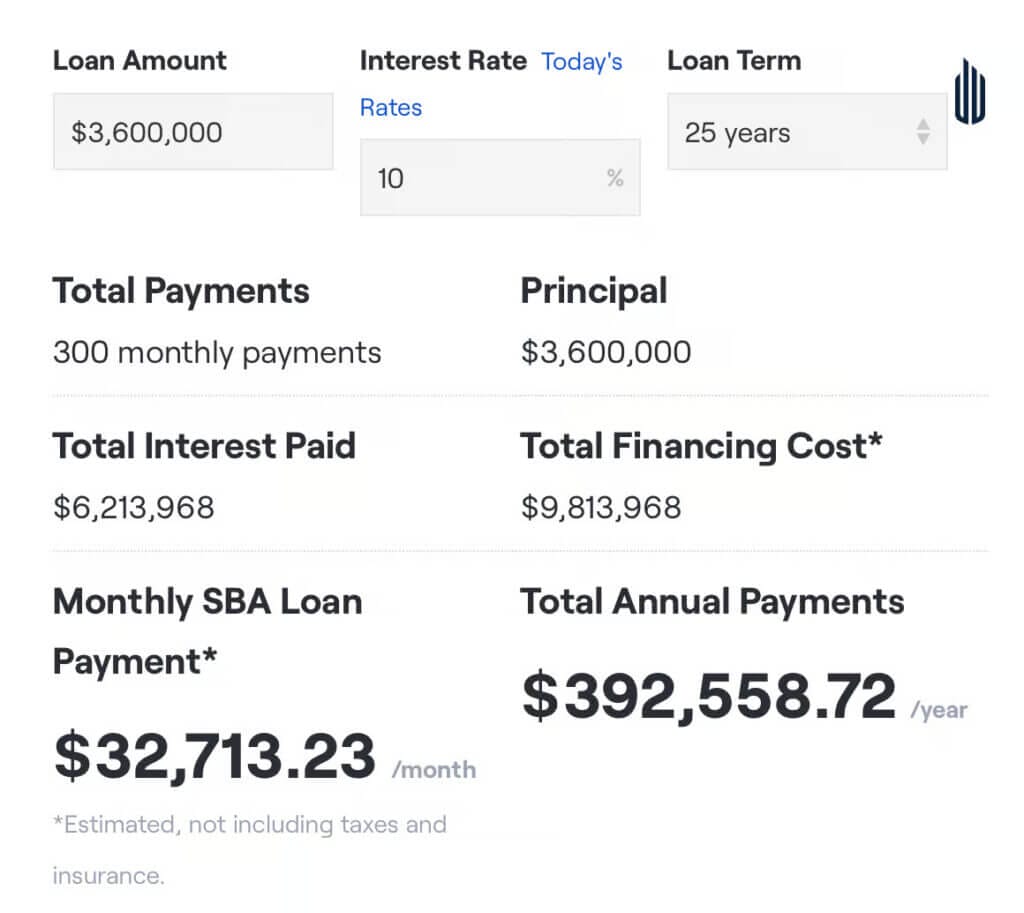

Let’s assume the building costs $3M.

The total sale price would be $4M ($1M for the gym + $3M real estate). Because SBA requires a 10% down payment, you’d need to come up with $400k.

Listen to our episode with Andrea Savard if you want creative ideas for finding money for a down payment.

Next, we need to figure out our debt service coverage ratio. We know the business does $25k/mo in cash flow. The listing also says that the business is paying $25k/mo in rent. If we owned the building, we wouldn’t be paying rent, so that amount is added to the total amount of cash flow the business generates.

So we know we have $50k/mo ($25k cash flow + $25k rent add back) to service the debt.

Now it’s time to whip out our calculator:

It would cost $33k/mo to borrow $3.6M from the SBA. Since the business generates $50k/mo in cash flow, our debt service ratio is 1.5—which is well above the required level.

So now you:

- Own the biz

- Own the real estate

- Pocket 6-figures of cash flow

- Build equity in the business

- Build equity in the real estate…

…BEFORE doing anything to increase profits

You can see how you can build wealth fast if you find the right deal.

The perfect deal

Here is what I’d look for if I wanted to become a gym owner again:

1/ A single-location gym that’s been around for 10+ years…

Research shows that if a business has been around for 10+ years, it’s way more likely to exist for another 10+ years versus a newer business. I’d also look for steady revenue and cash flow.

2/ …that generates $250k-500k in cash flow/yr…

I don’t want to buy myself a job. If a gym does $250k+ in cash flow, they likely have good systems and staff in place. And if it doesn’t, the business generates enough cash to hire a decent manager.

3/ …and sits on $3-4M of real estate.

Why pay rent to a landlord when you can be your own landlord and build equity in your building every month? Owning the real estate also gives you more optionality because you own two assets: the business and the real estate. If you get tired of operating the gym, you can sell the business, keep the real estate, and enjoy passive income every month.

A deal like this would get me pretty close to the $5M lending limit for a 7(a) loan and give me a decent shot of increasing my net worth by 5-10M over the next 10 years.

Hope this helps,

j

P.S. If you want to learn more about buying gyms and buildings, watch our full interview with Angelo Medici: