How to fast-track your retirement in 10 years or less

What’s up Gym World?

In my experience, the most successful gym owners usually follow one of two paths:

Path 1: nail down a profitable model and expand to multiple locations

Path 2: build a profitable location and then use the cashflow to buy real estate

Our latest guest, Stu Brauer, followed Path 2. He ran a CrossFit affiliate for 7 years before de-affiliating, rebranding, and buying a building to house a new concept.

He retired four years later at 35 years old.

Your gym won’t make you wealthy, but the cash you generate from your gym can.

Let’s break down how Stu was able to retire from running one gym.

There are five phases in the process:

Phase 1: Scratch and claw for survival

Timeline: 0-2 years | Goal: get profitable at any cost

The first few years after opening a gym are dicey.

You’re likely in debt, losing money every month, and working way too many hours.

To make it out of this phase, you need to build a revenue base and get profitable as fast as possible.

Some gym owners never leave this phase. At Two-Brain Business, we’ll often talk to gym owners who scraped by for 5-10 YEARS before asking for help. By the time they call us, it’s too late. If what you’re doing isn’t working after 24 months, FFS get some help.

The fastest way out of this phase is properly packaging and pricing your services, and taking a proactive approach to getting new clients.

Stuff like:

- DM-ing potential prospects

- Talking to people located near your town, &

- Asking your best clients for referrals

doesn’t cost money, is easy to do, and will get you to break even with little-to-no marketing skills. Remember: more conversations lead to more conversions.

Phase 2: Build up your cash flow

Timeline: 2-3 years | Goal: become bankable

The amount of money a bank will lend you is directly dependent on the cash flow your business generates.

So if your goal is to own real estate, avoid:

- buying a ton of expensive equipment

- taking on unnecessary debt

- opening multiple locations that could hurt the cash flow of your first location

- increasing your personal expenses

for the three years leading up to your purchase.

Think of every objectionable reason the bank would not give you a loan, and get those out of the way early.

For U.S. gym owners, your best bet is an SBA 7(a) loan or an SBA 504 loan. You can access up to $5M in capital, as long you have:

- A credit score of 650+

- No past bankruptcies

- Some business experience

- Enough cash flow to pay your loan

There are accountants out there actively telling gym owners to buy shit they don’t need to “avoid taxes.” This is bad advice if real estate is part of your retirement plan.

During phase 2, we want to build a thiccc stream of cash flow. There will be plenty of better tax write-offs down the road when you own a multi-million dollar building.

Phase 3: Plan your buy

Timeline: 0-2 years | Goal: work out your target market, building size, and financials

Here’s what you should consider before you buy a building:

Ideal location

You want to be positioned on the path of progress—which is jargon for the direction of development, gentrification, and/or economic growth of a city. If you invest ahead of all the deep-pocketed developers, you’ll experience the wealth-building superpowers of appreciation and leverage.

Pro tip: Stu listened to zoning hearings in his town to see where large developers were spending money.

Next month, we’re releasing an episode with a gym owner who bought a building for $300k. A developer wanted the space for a redevelopment project and offered him over $2M to GTFO.

Ideal size

One of the smartest parts of Stu’s plan was that he looked for a space that “had the potential to be more than a gym.”

His concept only required 3,000 square feet, but he bought a 10,500 sq ft facility and built out the remaining space to attract a brewery as a tenant.

What Stu did violated his loan agreement, but you can legally lease up to 49% of your space with an SBA loan.

A nice-sized building on the path of progress sets you up to get “lucky.”

A company loved Stu’s building so much that they offered him 4.5x his mortgage and expenses to lease up the entire space for 20 years. So Stu shut his gym down and now collects nearly $21,000/mo in “mailbox money.”

I know you’re probably saying, “well that’s great for Stu, but I’ll never be able to afford a multi-million dollar building.”

Nonsense! You read Gym World; anything is possible with a little planning.

So let’s figure out how you’re going to finance your building, so you too can get some mailbox money. Let’s break it down in two steps:

Step 1: Put together the downpayment

By now, you should have a general idea of the location and building size you’re looking for. That should also give you a general idea of what it’s going to cost.

The SBA is going to require a 10% downpayment. So if you’re looking at $2M building, for example, you’ll need to come up with $200k. Here are your options:

Option 1: Save up enough cash for a downpayment

This is the best-case scenario (see phase 2).

Option 2: Get an investor

Stu used an investor to help him buy his building.

The pitch was simple:

Because Stu was a biz owner, he could qualify for an SBA loan—which only requires a 10% downpayment and offers terms of up to 25 years. A traditional commercial loan requires a 30-35% down payment and usually a 5-10 year balloon payment.

Additionally, by working with Stu, the investor could avoid finding a tenant (Stu’s gym was the tenant) and paying leasing commissions (around 6% of the entire lease).

As a gym owner, you can provide the same value to an investor.

Step 2: Figure out how much space you can afford

To know how much building you can afford, you need to understand debt service coverage ratios (stay with me).

Banks use debt service coverage ratios to figure out how much debt you can take on.

If you’re buying real estate through the SBA, the ratio is 1:1—so to service $1 of debt payment, the business needs to generate $1 of cash flow.

This article breaks it down in further detail.

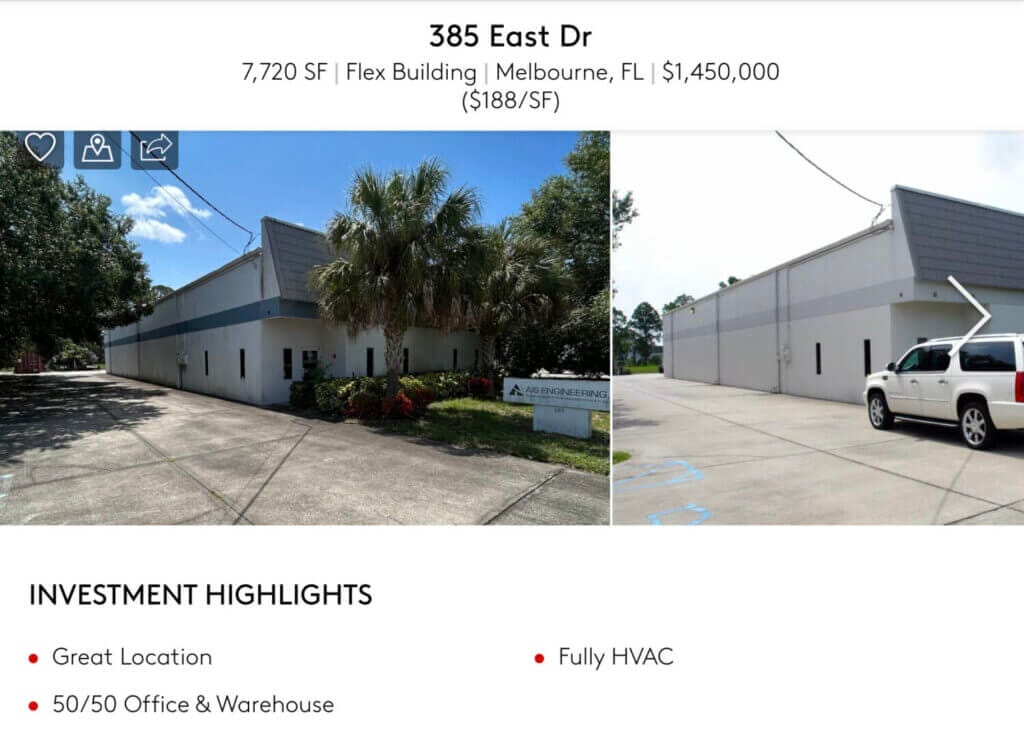

Let’s look at an example using an ad I saw for a building in Florida:

The asking price for the space is $1.45M.

Using SBA, you’ll need a 10% downpayment of $145k (10% of $1.45M), and the SBA should cover the remaining $1,305,000 IF your business meets the 1:1 debt service coverage ratio.

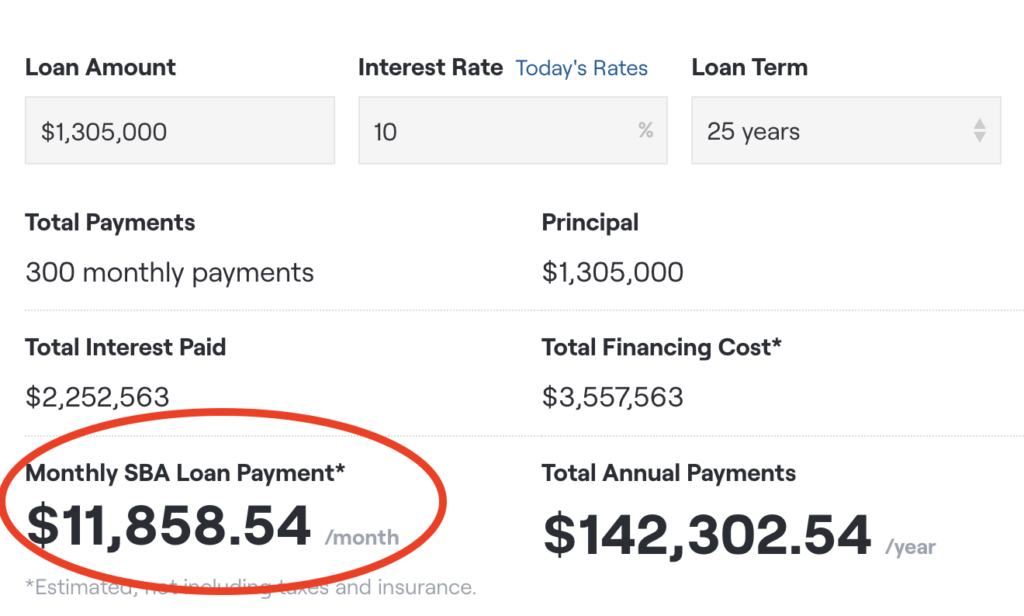

Let’s use this calculator to find out how much money your gym needs to generate:

Plug in those numbers, and you can see you’ll need $12k/mo in cash flow to cover $1,305,000 of debt. This is AFTER paying yourself a salary that’ll maintain your current lifestyle.

Two things to note:

- If you currently pay rent, add that back into your cash flow since you won’t be paying that anymore. You’re the landlord now, big shot.

- If you’re leasing part of the space, add that rent payment to your cash flow.

Phase 4: Buy your building

Timeline: 1-2 years | Goal: own an appreciating, cash-flowing asset

This will likely be the largest purchase of your life. Get yourself a good broker and a good lawyer—they’re worth many times more than what you will pay them.

It’s also important to keep in mind that the best deals are found off-market.

So if you see a building you like, try knocking on their doors and asking if the landlord or current tenant would be interested in an offer.

Stu did this with two properties he bought and says there was way less competition that way.

Buying a building before you’re ready

Sometimes the perfect space comes up before you’re bankable. If that’s the case, you can use creative financing.

The most common is owner financing. This is when the current owner acts as the bank and finances the building for you.

Here’s an example of a location offering owner financing at “an attractive rate” with a 25% down payment:

Phase 5: Wait for good things to happen

Timeline: 1-3 years | Goal: collect cash flow and wait for appreciation to do its thing

Many of the wealthiest gym owners that have come on Gym World made more money in real estate than they did running their gym.

I’ve got the receipts:

- When Stu leased his space to a brewery tenant, he increased his rental income by over $16k/mo and retired at 35. He did this all in under 5 years, which sounds extreme, but he says it’s possible for gym owners to do it in at least 10.

- Andrea Savard never even ran her gym out of the building that she bought. Instead, she rented the space to a Cannabis company, sold it to an eager investor, and wound up with a $1.8M profit in 10 months.

- And coming soon to Gym World, you’ll hear how one gym owner made over $2M from a building he bought for $300k AND got a new space AND three years of free rent.

If you want to make commercial real estate part of your wealth plan, watch or listen to Stu’s interview to get a full breakdown of his strategy.

Until next week,

j